Private Equity

The rise of tech, the decline of oil and more private equity charts from 2020

December 23, 2020

It was another year full of headline-grabbing buyouts and massive new funds for the US private equity industry. As we all know, it was also a year full of unexpected and unprecedented events. The arrival of the coronavirus crisis in March had an explosive effect across the private markets, and buyout investors spent the rest of 2020 dealing with the shockwaves.

One major development that emerged this year was a surge in PE-backed IPOs. Here are five other trends that show how the US private equity industry has shifted over the past 12 months:

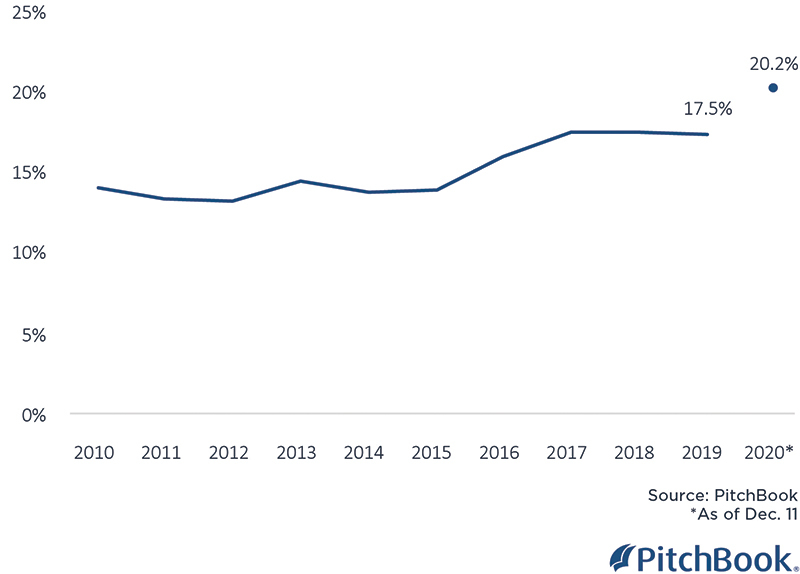

Private equity firms have shown a growing embrace of the tech industry over the past decade or so, following in the footsteps of industry pioneers Silver Lake, Thoma Bravo and Vista Equity Partners. That continued in 2020, as the percentage of US PE investments in the information technology sector reached an all-time high. Investors flocked to tech companies of all kinds this year, with a surge in tech stocks also serving as a major factor in the public market's surprising resilience amid the pandemic.

The pandemic has created all kinds of uncertainty for investors. And that uncertainty has helped drive down the median price of buyouts, with many firms opting to hold onto some of their substantial dry powder and pursue smaller purchases—reversing a shift toward larger buyouts that had been building the past few years. This year's transition is also reflected by the fact that add-ons are on track to account for their highest percentage ever of all US private equity investments, with these add-ons often representing smaller and simpler deals than new platform investments.

March was the most chaotic month of the year for the financial markets, as stocks plunged and investors were forced to confront the new realities of the building pandemic. That fact is reflected in the sorts of returns generated by US private equity funds, as the industry's IRR for the first quarter dipped to -6.4%, falling into negative territory for just the third time in the past 10-plus years.

Prices have been rising steadily in the PE industry for the past couple of years. But they reached a recent high in Q2, when the upheaval of the pandemic helped drive the median enterprise value-to-EBITDA multiple up to 15.2 times on a rolling four-quarter basis. The median equity-to-EBITDA multiple alone soared to 8.4x for that quarter, approaching combined EV-to-EBITDA multiples from 2015.

Featured image via Sergii Iaremenko//Getty Images

One major development that emerged this year was a surge in PE-backed IPOs. Here are five other trends that show how the US private equity industry has shifted over the past 12 months:

IT investments as a percentage of all PE deals in the US

Private equity firms have shown a growing embrace of the tech industry over the past decade or so, following in the footsteps of industry pioneers Silver Lake, Thoma Bravo and Vista Equity Partners. That continued in 2020, as the percentage of US PE investments in the information technology sector reached an all-time high. Investors flocked to tech companies of all kinds this year, with a surge in tech stocks also serving as a major factor in the public market's surprising resilience amid the pandemic.

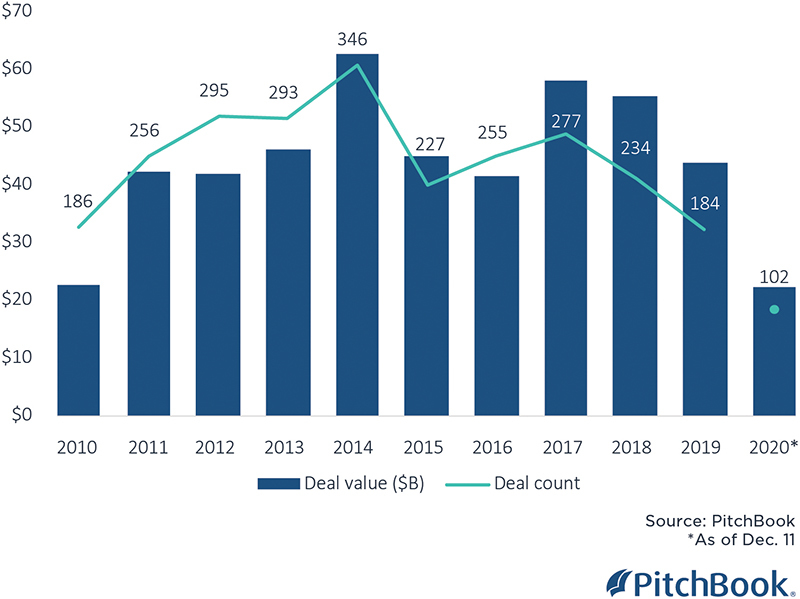

US PE deal activity in the oil and gas sector

The price of West Texas Intermediate famously went into negative territory in April. It was the starkest symbol of the severe effects the pandemic wrought on the oil and gas sector, as decreased air travel and other factors drove down demand. Private equity firms had already been backing away from US oil and gas investments in recent years after activity spiked in the first part of the decade. But the pandemic proved a catalyst, with deal value plunging 49% year-over-year through Dec. 11 and deal count declining 45%.

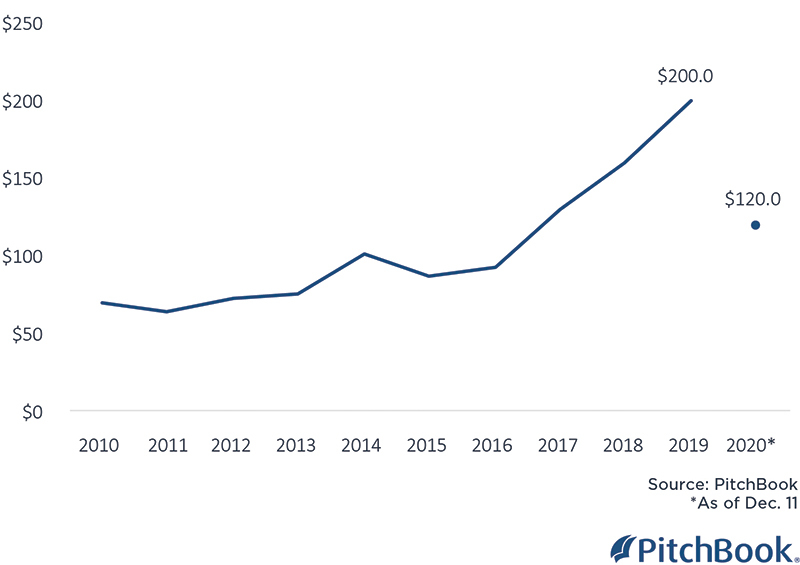

Median size of buyouts in the US ($M)

The pandemic has created all kinds of uncertainty for investors. And that uncertainty has helped drive down the median price of buyouts, with many firms opting to hold onto some of their substantial dry powder and pursue smaller purchases—reversing a shift toward larger buyouts that had been building the past few years. This year's transition is also reflected by the fact that add-ons are on track to account for their highest percentage ever of all US private equity investments, with these add-ons often representing smaller and simpler deals than new platform investments.

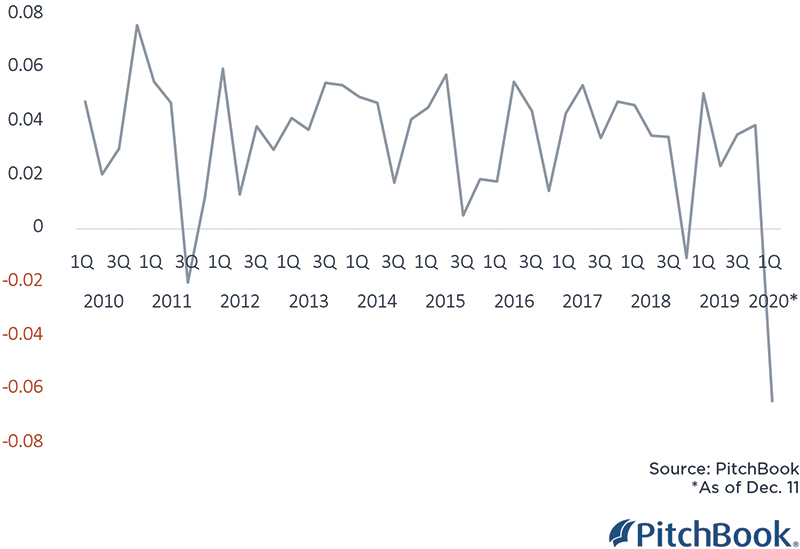

Quarterly IRR for US PE funds

March was the most chaotic month of the year for the financial markets, as stocks plunged and investors were forced to confront the new realities of the building pandemic. That fact is reflected in the sorts of returns generated by US private equity funds, as the industry's IRR for the first quarter dipped to -6.4%, falling into negative territory for just the third time in the past 10-plus years.

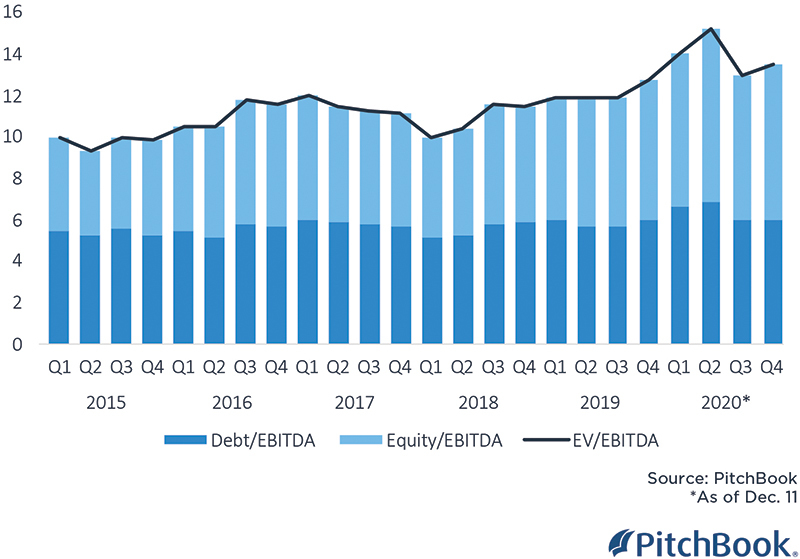

Rolling four-quarter median of buyout EV/EBITDA multiples in the US

Prices have been rising steadily in the PE industry for the past couple of years. But they reached a recent high in Q2, when the upheaval of the pandemic helped drive the median enterprise value-to-EBITDA multiple up to 15.2 times on a rolling four-quarter basis. The median equity-to-EBITDA multiple alone soared to 8.4x for that quarter, approaching combined EV-to-EBITDA multiples from 2015.

Featured image via Sergii Iaremenko//Getty Images

Comments:

Thanks for commenting

Our team will review your remarks prior to publishing.

Please check back soon to see them live.