10 charts capturing the European PE market

November 13, 2018

With the end of 2018 in sight, European PE dealmaking in 3Q has fallen short, registering the weakest quarterly results so far this year. Across the industry, dealmaking, fundraising and exits all lag behind previous quarters, but what lies behind this phenomenon?

We took a look at ten charts from our latest European PE Breakdown outlining the current state of the private equity industry.

We took a look at ten charts from our latest European PE Breakdown outlining the current state of the private equity industry.

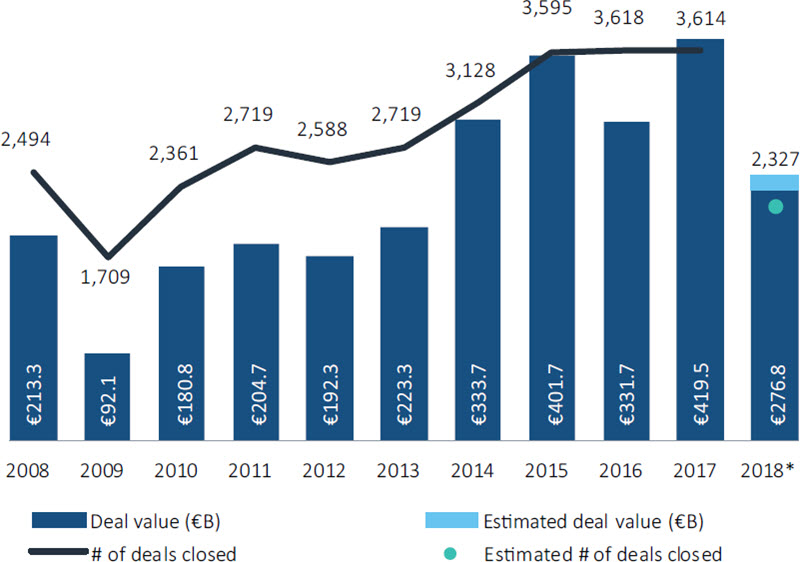

3Q lags but 2018 on track for good year

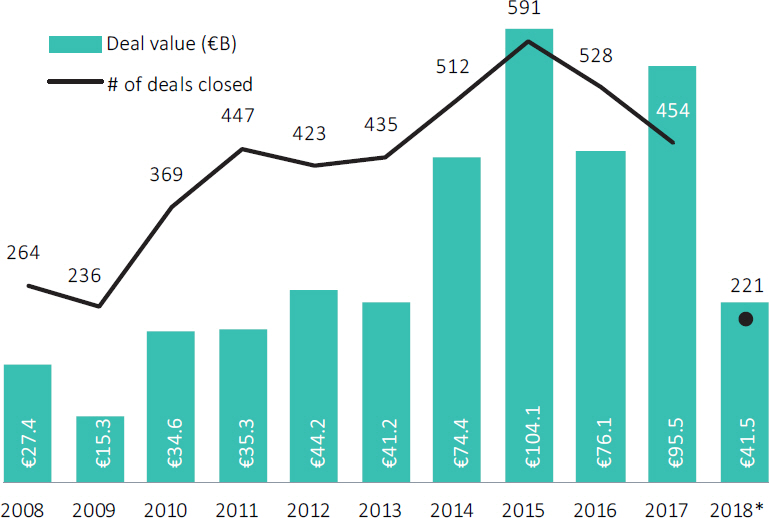

The third quarter saw some 731 transactions take place with a combined value of €82.6 billion, bringing the totals for the first nine months to 2,327 deals worth €276.8 billion—a 14.8% and 15.3% decrease, respectively, compared with the first three quarters of 2017. A lack of deals worth more than €2.5 billion could account for the drop in value; only eight have been completed thus far, compared with 14 during the same period in 2017.Bolt-ons stay put

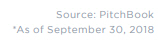

The proportion of bolt-on transactions has remained at a consistent level, accounting for around half of all PE buyouts—equating to 845 completed deals in 2018. While the percentage of bolt-ons has lingered around the 50% mark since 2011, this type of transaction may become more prevalent as GPs find that funds with platform companies that see higher levels of bolt-on activity have been associated with better performance.IT increases its presence

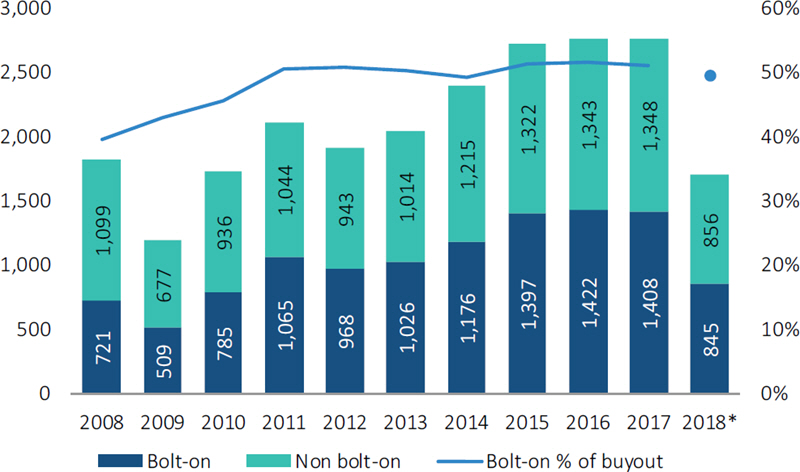

For the fifth consecutive year, deals within the IT sector have been taking up an increasing share of total PE transactions. B2B is still the preeminent sector, with the proportion of deals in this area remaining stable at about a third of overall activity since 2012. Meanwhile, investments in both healthcare and financial services have seen a slight decrease as a proportion of overall deals.UK & Ireland on top

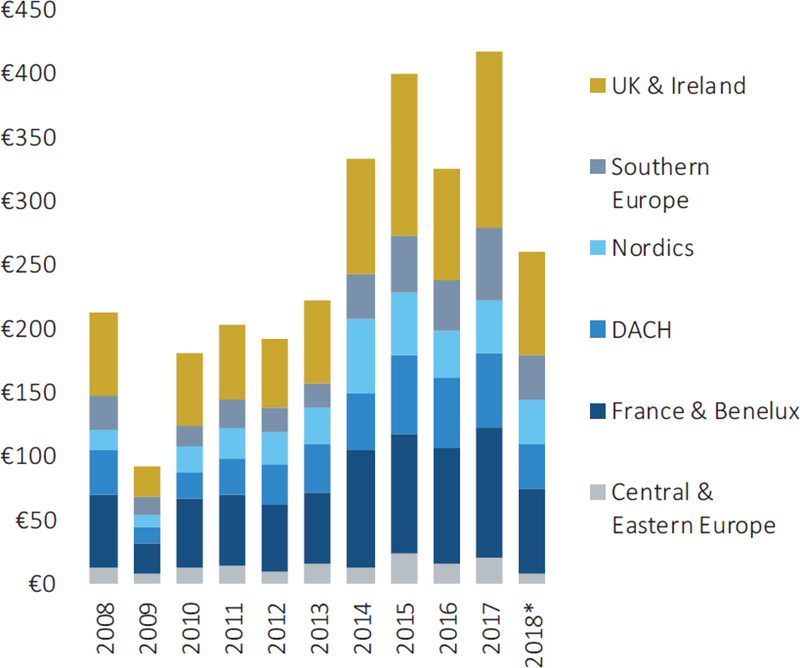

The UK & Ireland continues to lay claim to European PE's crown in terms of both volume and value, although the France and Benelux region follows not too far behind. By contrast, this year has seen Central & Eastern Europe and the DACH regions lose some of their market share.Spotlight on carveouts

In keeping with the overall trend of PE deals, the number of carveouts has also failed to keep up with previous years. So far this year, 221 transactions have closed worth €41.5 billion. However, of the deals that are left, carveouts are appearing more commonly on the menu.PE firms carry a bigger load

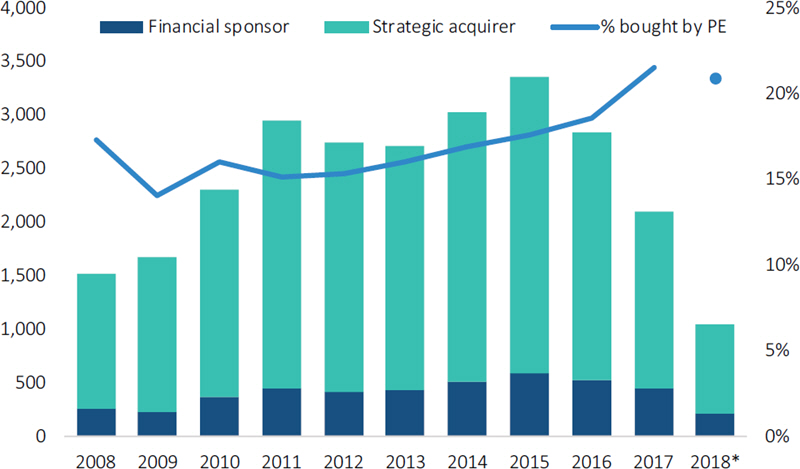

Despite being on a downtrend, private equity investors have been increasing their share of overall carveout deals. PE accounted for 20.9% of all deals completed so far this year, compared with 14% in 2009, as investors in the industry represent a growing proportion of buyers in the broader M&A market.Exits come up short

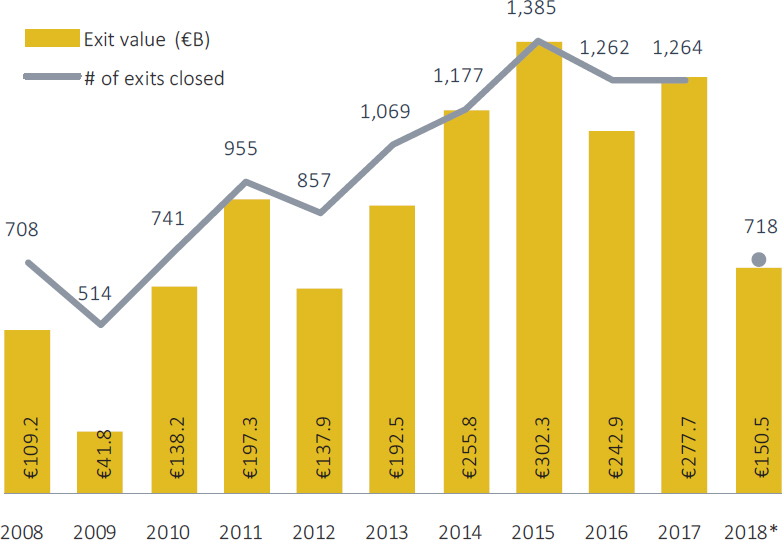

GPs have exited just 718 companies for a combined €150.5 billion so far this year, putting 2018 on pace to fall far behind last year's 1,264 exits worth €277.7 billion. This may be explained by the fact that sizable exits have been a rarity, as deal values in the €2.5 billion-plus bracket dropped to their lowest levels since 2009.Secondary is the new primary

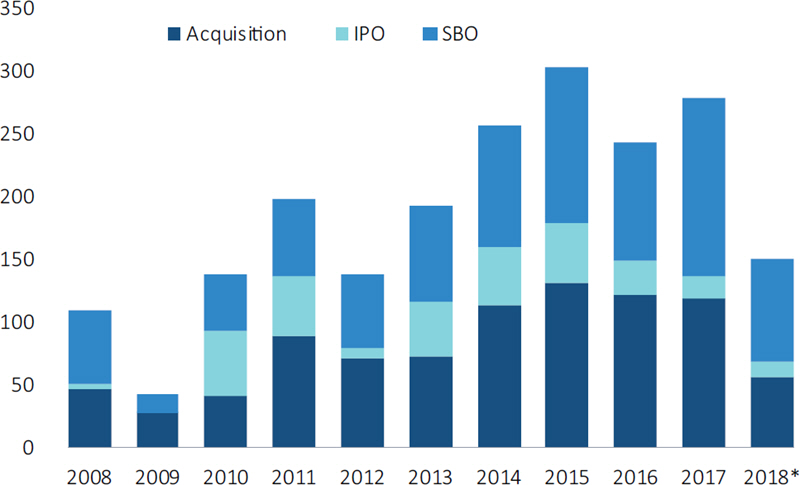

Already lacking in exit activity, 3Q saw only five PE-backed companies go public, despite the two preceding quarters having a combined 34 IPOs. Secondary buyouts were by far the most common exit type, accounting—for the first time—for the majority of total exit value and count, with 375 deals worth €82.7 billion through 3Q this year.Fundraising catches up

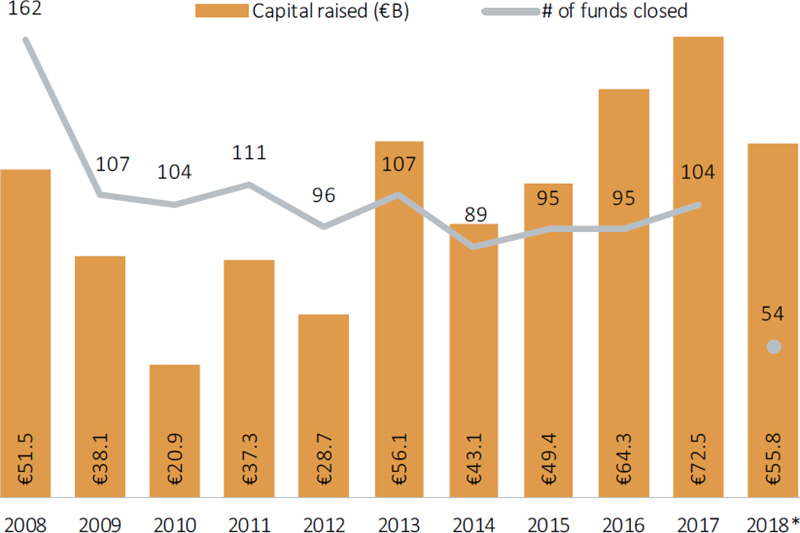

This year has seen a healthy level of fundraising so far, despite a slow third quarter, with PE firms collecting €55.8 billion for 54 vehicles overall in the first nine months of 2018. It is important to note that the vast majority of this capital originated from 1Q fund closes, with the two following quarters seeing a dramatic decrease in activity. However, 2018 is set to be on par with last year's record-setting total in terms of capital commitments. Whether the last two quarters suggest the end of the party, however, remains to be seen.The year of the mega-fund

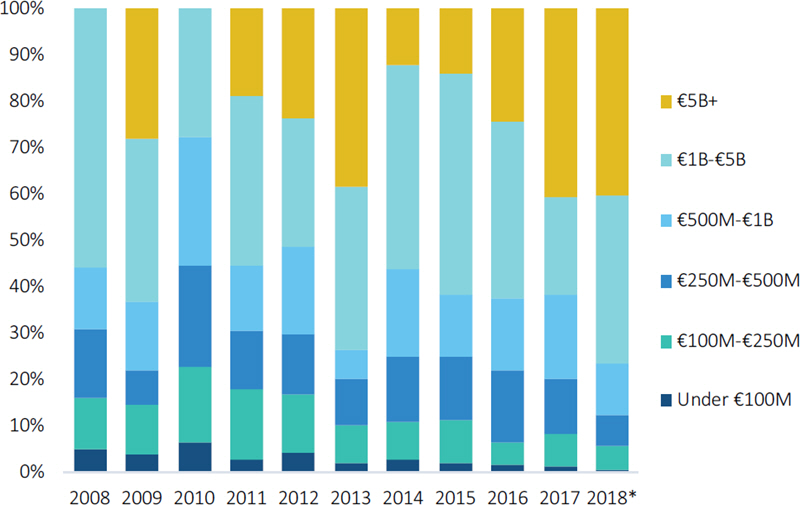

Despite deal counts and value decreasing, fund sizes have continued to swell. Billion-euro funds hold a record share of capital raised for funds this year with 77.9% of the total going to these large vehicles. On top of that, some 41% of capital was committed to funds worth over €5 billion.Looking for the full report? Check out our 3Q 2018 European PE Breakdown

Comments:

Thanks for commenting

Our team will review your remarks prior to publishing.

Please check back soon to see them live.